I have always had a simple problem with home finance and budgeting software: It doesn’t care whether you have money in the bank or not. For anyone just beginning budgeting, that is a disaster in the making.

The Problem with Budget Reports

Let’s say I want to have a budget for gas for our two cars. Looking back over last year, I can see that Christina and I spent an average of $204.82 per month on gas. If I set that amount as my monthly budget on day one of this year, I could spend $204 on the first day of the month and our home finance software would happily tell me I am under budget. Woohoo!

The problem for most people is that they don’t have that whole $204.82 available on day one of any given month. Almost 60% of Americans live paycheck-to-paycheck, according to a 2019 Charles Schwab survey. Anyone basing personal finance decisions on a simple budget report can find themselves in hot water quickly.

The Evolution of a Budget

That basic problem – trying to live by a budget when the money isn’t available in advance – caused us a lot of trouble early in our marriage. Like many, we lived by our checkbook balance. If our balance was insufficient we would use credit (and pray to God there were no NSF charges from some forgotten expenditure). Financially, we began spiraling downward into significant credit card debt.

We lived in that reality for many years before getting our personal finances under control using a stone-age method: envelope budgeting. Micro-explanation: you spend only what you actually have on-hand.

Even after getting to the point that I could have a month’s expenses available in advance – when a classic budget could be functional – I still loved the simplicity of the envelope system. With a simple balance report, I knew at a glance exactly how much money was available for Gas, Groceries, and every other budget line at any time.

Early-on, I kept track of our envelope budget in Excel. It was effective but time-consuming. I used receipts to track expenses (which occasionally left gaps when we would misplace a receipt or not get one at all), and then updated the envelope balances in Excel each week.

I made the (partial) switch to financial software when Microsoft started giving away copies of Microsoft Money with Windows ’95. With its ability to import transactions from financial institutions, MS Money essentially replaced receipts as my system of record.

Enter the challenge: How to get rid of my manual Excel budget and use the automated tools at hand so I could spend less time keeping track of our money? I found a solution in MS Money, and later in Quicken, by treating my paycheck in an unusual way.

The Hack: Treating Income as Negative Expenses

MS Money, Quicken, and any other financial package will allow you to report on your expenses by category for a given period, but that just tells you how much you’ve spent by category – not how much is left in your envelopes. My solution undermines some of the original purpose of financial software (e.g. to produce financials showing income and expenses), but it serves the purpose I need the most: To tell me where I stand. I can filter data to serve other purposes.

For my accountant friends: This is a bit like (ok, exactly like) posting everything directly to a balance sheet account. The trouble is: Most home finance software doesn’t work that way, and isn’t the point that you shouldn’t have to be an accountant to keep track of your home budget?

The basic setup outline:

- Create Expense Categories for each budget (envelope).

- Split each deposit into each budget when recording them (these appear as negative expenses).

- Record expenses into each budget line as they occur.

- Create a report showing the running balance from the beginning of time by expense category.

A Simplified Example

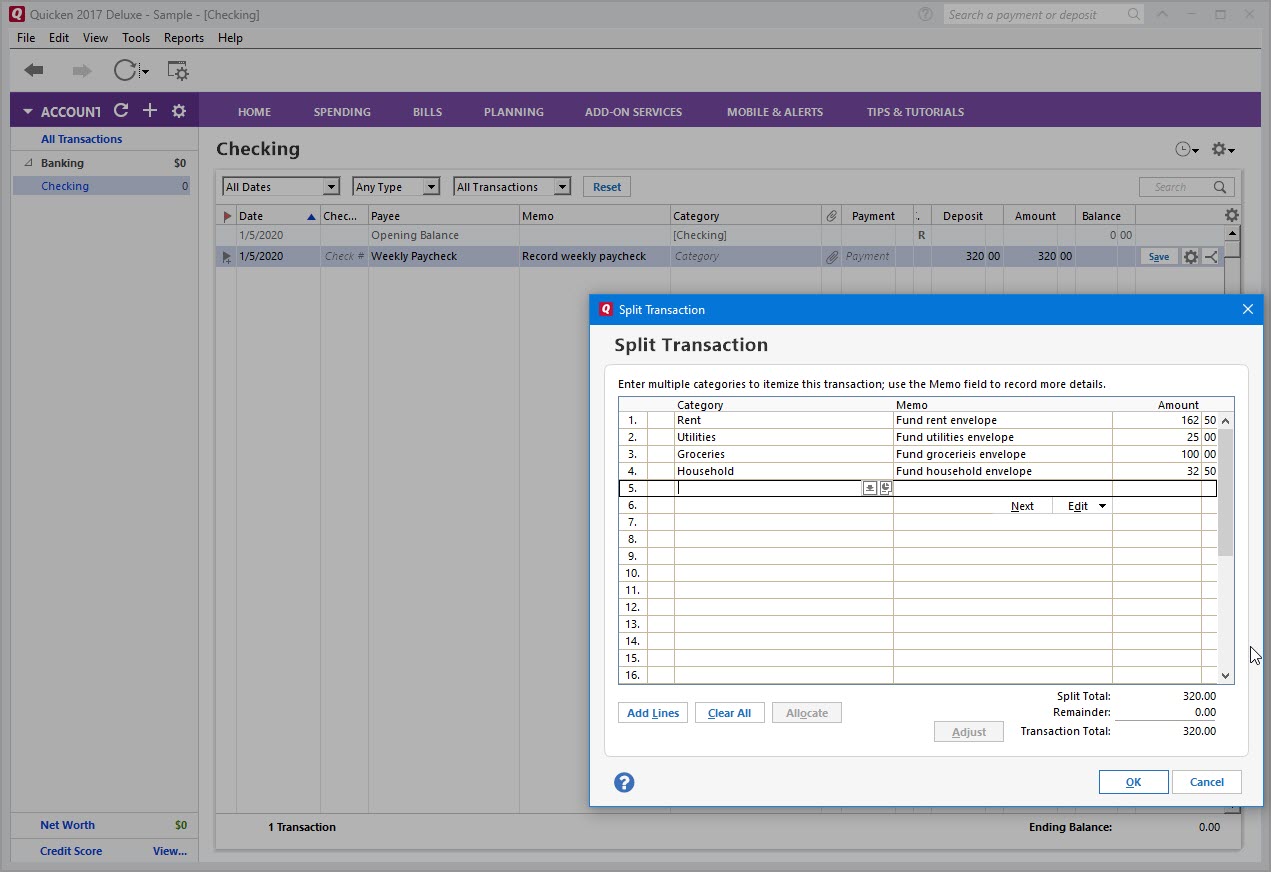

Let’s say I make $10 an hour, am paid weekly, and lose about 25% to taxes, leaving take-home pay of $320 per week. For budgeting purposes, I am going to assume ‘weekly’ means 4 times per month.

PRO TIP: If you are paid weekly or bi-weekly, and if you can at all manage it, calculate your budget as if you were paid 4 (if weekly) or 2 (if bi-weekly) times each month. You will end up with ‘extra’ checks each year that you can use as needed. I often used that method for funding Christmas and vacations.

Let’s also assume a simplified (and totally unrealistic) budget, based on take home of $320 four times per month (total $1,280/month).

- Rent: $650/month. Weekly budget = $650/4 = $162.50

- Utilities: $100/month. Weekly budget = $25.

- Groceries, etc: $400/month. Weekly budget = $100.

- Household (everything else): $130. Weekly budget = $32.50

SETTING IT UP

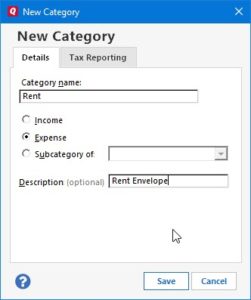

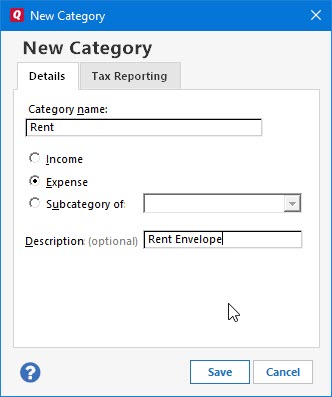

- Create Expense Categories for each of your budget areas. In Quicken 2017, the process is:

- Tools -> Categories -> New Category

- Fill in the form, selecting “Expense” as the type, and “Save”.

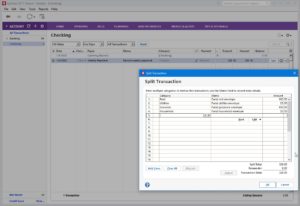

- Post Deposits Into Budgets:

- On pay day, record your pay as a $320 deposit and “split” it among those Expense Categories. In Quicken, it looks like this:

- On pay day, record your pay as a $320 deposit and “split” it among those Expense Categories. In Quicken, it looks like this:

- Record expenses as you spend money and pay bills.

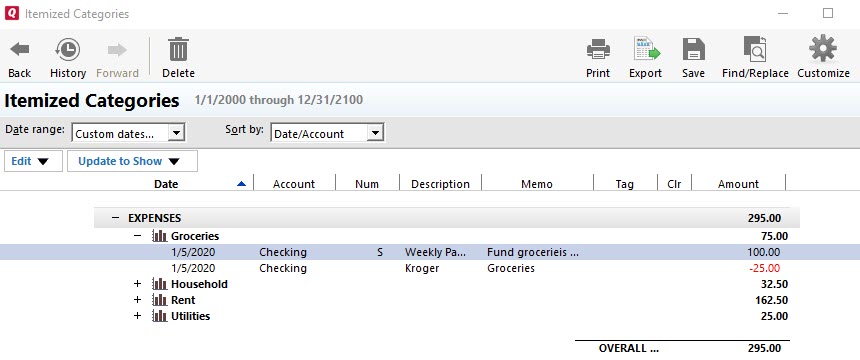

- Create a report of running balances. Example for Quicken 2017:

- Reports -> Spending -> Itemized Categories

- The example below shows the “Groceries” category expanded so you can see the entries.

- The bold numbers are my envelope balances.

- Note my date range. I used “Customize” to set an all-inclusive range. You’ll find that helpful if your file has more than one year in of detail.

Et Voila

There are many other software packages that are more suited for Envelope budgeting, but I work with what I have – and switching software can be a major time suck. In the meantime if you have access to Quicken or some other popular personal finance package, this method can get you the information you need to control your budget.

I intend to try out YNAB or EveryDollar after I read up on some reviews. I think I can streamline my current system, but like I said: Switching software can be a major time suck.